Zimbabwe’s telecom sector is growing. That part is obvious.

What is less obvious and far more important is this: the industry’s core economics are starting to crack under the weight of that growth. The latest Postal and Telecommunications Regulatory Authority of Zimbabwe (POTRAZ) Fourth Quarter 2025 Sector Performance Report paints a picture of a market that is expanding rapidly on the surface, while quietly struggling underneath. Data usage is climbing. Infrastructure investment is accelerating. But profitability is tightening, and the arrival of Starlink is beginning to reshape who actually captures the most valuable users. This is no longer just a growth story. It is a structural shift.

The Data Explosion Is Undeniable

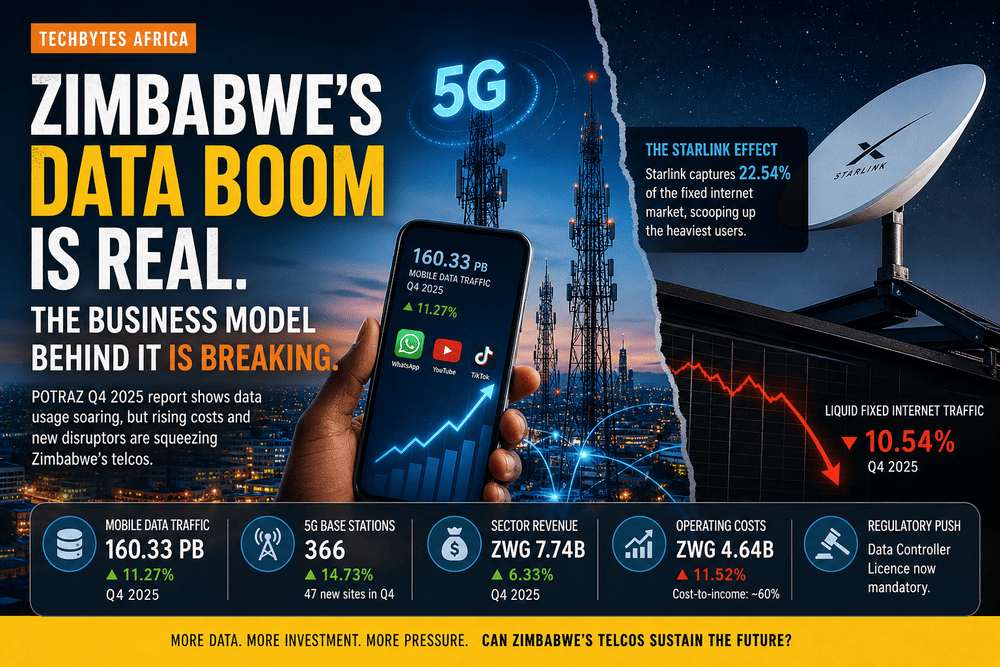

Zimbabwe’s mobile internet traffic hit 160.33 petabytes in Q4 2025, an 11.27% jump in just three months. That kind of growth does not happen in isolation. It reflects a behavioral shift. Users are no longer just messaging. They are streaming, scrolling, uploading, and working online. Platforms like WhatsApp, YouTube, and TikTok are now baseline utilities, not optional apps. Operators are responding the only way they can. Build more capacity. 5G infrastructure expanded by 14.73%, with 47 new base stations deployed in a single quarter. But here is the catch: only 18.9% of the population can actually access that network. So the sector is investing heavily in infrastructure that most of the market still cannot use. That gap matters.

Growth Is Happening. Profitability Isn’t Keeping Up

Revenue grew. On paper, that looks like progress. Mobile network operators generated ZWG 7.74 billion, up 6.33%. But operating costs rose almost twice as fast, climbing 11.52% to ZWG 4.64 billion. That imbalance is not a rounding error. It is a warning sign. A cost-to-income ratio approaching 60% means operators are spending more and more just to keep the network running, let alone expand it. And they are not slowing down on investment. Capital expenditure more than doubled to ZWG 1.08 billion. This is the uncomfortable truth: The more data people use, the more expensive the system becomes to sustain. And right now, pricing models are not catching up.

Starlink Isn’t Just Competing. It’s Rewriting the Market

The biggest disruption in this report is not local. Starlink has quietly captured 22.54% of the fixed internet market, second only to Liquid Intelligent Technologies. But the more important detail is not market share. It is who is switching. Fibre subscriptions are still growing. On paper, that suggests stability. But traffic on Liquid’s network dropped 10.54% in the same period. That contradiction tells you everything. High-usage customers, the ones who stream heavily, work remotely, and consume large volumes of data, are moving to Starlink. What remains on fibre is lighter usage. In simple terms: The most valuable users are leaving traditional networks. That is not competition. That is erosion of the premium segment.

Voice Is Holding On. SMS Is Not

Voice traffic grew 9.04% to 5.07 billion minutes, largely driven by Econet Wireless Zimbabwe and aggressive bundle strategies. That tells you something important. Price incentives still work. But SMS continues its steady decline, dropping 3.49%. Messaging has already been replaced by data-based platforms. That shift is permanent. Operators are no longer selling communication. They are selling access.

Regulation Is Catching Up to the Reality

As the digital economy expands, POTRAZ is tightening oversight. The push for mandatory Data Controller Licences signals a shift toward stricter data governance. This is not just compliance for its own sake. It is a recognition that data is now central to the economy. But regulation introduces another layer of cost and complexity at a time when margins are already under pressure.